Consumer behavior and demand play a crucial role in shaping the dynamics of market economies. Understanding how consumers make decisions and how their preferences affect market demand is essential for businesses to succeed. In Chapter 4 demand worksheet, we explore the various factors that influence consumer behavior and delve into the concept of elasticity to measure the responsiveness of demand.

One of the key topics covered in the Chapter 4 demand worksheet is the law of demand, which states that as the price of a good or service increases, the quantity demanded by consumers decreases, ceteris paribus. Through the worksheet, students gain insights into the reasons behind this inverse relationship between price and quantity demanded, such as income effect, substitution effect, and the law of diminishing marginal utility.

The worksheet also introduces students to the concept of elasticity of demand, which measures the responsiveness of quantity demanded to changes in price. It explores different types of demand elasticity, including price elasticity of demand, income elasticity of demand, and cross elasticity of demand. Understanding these concepts helps businesses make informed decisions about pricing, production, and marketing strategies.

Overall, the Chapter 4 demand worksheet provides students with a comprehensive understanding of consumer behavior and market demand. By answering a range of questions and exercises, students develop critical thinking skills and improve their ability to analyze and predict consumer choices. This knowledge is invaluable for businesses looking to optimize their operations and effectively meet the needs and wants of their target market.

Chapter 4 Demand Worksheet Answers

In Chapter 4 of the economics textbook, students were tasked with completing a demand worksheet that focused on understanding the concept of demand and its determinants. The worksheet consisted of various questions and scenarios that required students to apply their knowledge of demand to analyze and interpret the situations given.

The answers to the worksheet are as follows:

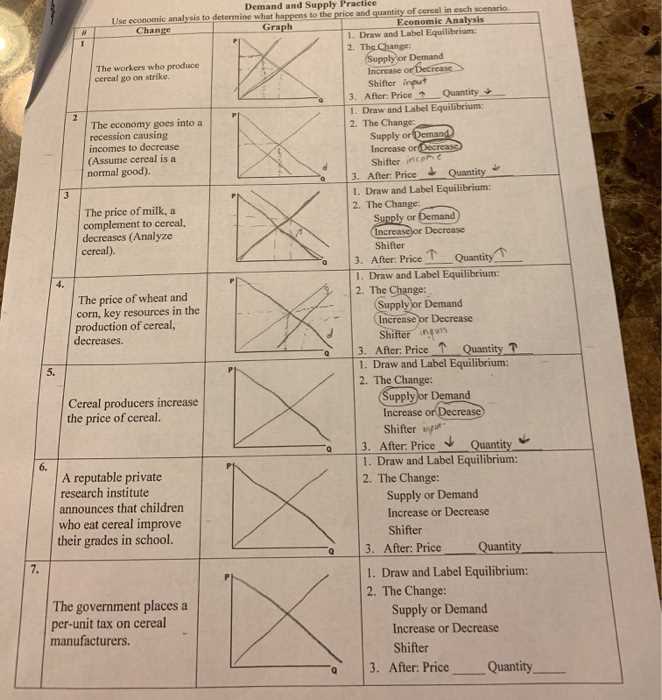

- The law of demand states that as the price of a good or service increases, the quantity demanded for that good or service decreases. This is due to the inverse relationship between price and quantity demanded.

- The determinants of demand include:

- Price of the good or service: A higher price will usually result in a decrease in demand, while a lower price will lead to an increase in demand.

- Income of consumers: An increase in income will generally lead to an increase in demand for normal goods, while a decrease in income may result in a decrease in demand.

- Tastes and preferences of consumers: Changes in consumer preferences can impact demand. For example, if a new fashion trend emerges, it may lead to an increase in demand for clothing items related to that trend.

- Price of related goods: The prices of substitute goods and complementary goods can influence demand. When the price of a substitute good increases, demand for the original good may increase. Conversely, when the price of a complementary good increases, demand for the original good may decrease.

- Expectations of future prices and income: Expectations about future prices and income can impact current demand. If consumers believe that prices will increase in the future, they may increase their current demand to avoid higher prices later.

- The concept of elasticity of demand was also covered in the worksheet. Elasticity of demand measures the responsiveness of quantity demanded to changes in price. If demand is elastic, a small change in price will lead to a proportionally larger change in quantity demanded. In contrast, if demand is inelastic, a change in price will result in a relatively smaller change in quantity demanded.

By completing the demand worksheet and understanding the answers, students gain a comprehensive understanding of demand and its determinants, allowing them to analyze real-world situations and make informed economic decisions.

Understanding Demand

Demand is a fundamental concept in economics that refers to the quantity of a good or service that consumers are willing and able to purchase at a given price. It represents the relationship between the price of a product and the quantity that consumers are willing to buy. Understanding demand is crucial for businesses as it helps them determine the optimal level of production and pricing strategies to maximize their profits.

There are several factors that influence demand. First and foremost is price. Generally, as the price of a product decreases, the quantity demanded increases, and vice versa. This is known as the law of demand. However, demand is not solely determined by price. Other factors such as consumer income, taste and preferences, the availability of substitute goods, and consumer expectations also play a significant role.

When analyzing demand, economists often use a demand curve to visualize the relationship between price and quantity demanded. The demand curve slopes downward from left to right, indicating that as the price decreases, the quantity demanded increases. This inverse relationship reflects the law of demand mentioned earlier. The demand curve can shift to the left or right depending on changes in the factors that influence demand.

Understanding demand is essential for businesses to make informed decisions about pricing, production, and marketing. By analyzing consumer behavior and market trends, businesses can accurately predict demand and adjust their strategies accordingly. Additionally, understanding the concept of elasticity of demand helps businesses determine the sensitivity of demand to changes in price, allowing them to set prices that maximize revenue and profits. Overall, a comprehensive understanding of demand is crucial for businesses to succeed in today’s competitive market.

Factors Influencing Demand

The demand for a product is influenced by various factors that can either increase or decrease consumer interest and willingness to purchase. Understanding these factors is crucial for businesses as they help in identifying the key drivers of demand and formulating effective marketing strategies. Some of the major factors influencing demand are:

- Price: Price is one of the most important factors that influence demand. Generally, when the price of a product decreases, the demand for it increases, and vice versa. Consumers tend to buy more of a product when it becomes affordable.

- Income: The income of consumers plays a significant role in influencing demand. When consumers have higher disposable income, they are more likely to spend on goods and services, resulting in an increase in demand. Conversely, during periods of economic recession or job losses, demand may decrease as people have less money to spend.

- Consumer preferences: Individual preferences and tastes also influence demand. Consumers have different preferences when it comes to color, design, functionality, and quality of products. Businesses need to understand these preferences and tailor their offerings accordingly to meet customer demands.

- Population: The size and composition of the population also impact demand. A larger population generally leads to higher demand, as there are more potential consumers. Furthermore, changes in demographics, such as an aging population or an increase in the number of young people, can also affect demand for specific products or services.

- Advertising and marketing: Effective advertising and marketing campaigns can significantly influence demand. By creating awareness and highlighting the benefits of a product, businesses can stimulate consumer interest and desire for the product, ultimately increasing demand.

- Competition: The level of competition in the market can impact demand. When there are multiple competitors offering similar products, consumers have more options to choose from. This increases the pressure on businesses to differentiate their offerings and attract customers, leading to fluctuations in demand.

By considering these factors and monitoring changes in consumer behavior and market trends, businesses can make informed decisions to meet customer demands and maintain a competitive edge.

Law of Demand

The law of demand states that there is a negative relationship between the price of a good or service and the quantity demanded by consumers, all else being equal. This means that as the price of a good or service increases, the quantity demanded by consumers will decrease, and vice versa. The law of demand is one of the fundamental principles in economics and is based on the observation that people tend to buy less of a good or service when its price increases because they have a limited amount of income to spend.

One of the main reasons behind the law of demand is the principle of diminishing marginal utility. As individuals consume more of a good or service, the additional satisfaction or utility they derive from each additional unit consumed tends to diminish. This means that as the price of a good or service increases, the marginal utility derived from consuming it decreases, leading consumers to demand less of it.

It is important to note that the law of demand assumes that all other factors influencing demand, such as consumer preferences, income levels, and the prices of related goods, remain constant. However, in the real world, these factors often change, leading to shifts in the demand curve. For example, if consumers’ income levels increase, they may be willing to buy more of a good or service at any given price, which would shift the demand curve to the right.

In conclusion, the law of demand is a fundamental principle in economics that explains the relationship between the price of a good or service and the quantity demanded by consumers. By understanding this law, economists and businesses can make predictions about consumer behavior and adjust their pricing and marketing strategies accordingly.

Elasticity of Demand

Elasticity of demand is a measure of how responsive the quantity demanded of a good is to changes in its price. In other words, it indicates how much the demand for a product will change when its price changes. The concept of elasticity is crucial for businesses and policymakers as it helps them understand the sensitivity of consumers to price changes and make decisions regarding pricing and production.

The formula for calculating price elasticity of demand is:

Elasticity of Demand = (% Change in Quantity Demanded) / (% Change in Price)

There are three types of elasticity of demand: elastic, inelastic, and unitary elastic. When demand is elastic, it means that a small change in price will result in a proportionally larger change in quantity demanded. Conversely, when demand is inelastic, a change in price will have only a small effect on the quantity demanded. Unitary elastic demand is when the percent change in quantity demanded is exactly equal to the percent change in price.

The elasticity of demand is influenced by several factors, including the availability of substitute products, the necessity of the product, and the percentage of income spent on the product. For example, if a good has many substitutes available, consumers are more likely to switch to a different product if its price increases, making the demand more elastic. On the other hand, if a good is essential or constitutes a small percentage of consumers’ income, the demand will be less elastic as consumers are less likely to change their consumption habits in response to price changes.

In conclusion, understanding the elasticity of demand is critical for businesses and policymakers to make informed decisions about pricing and production. By knowing how consumers will respond to changes in price, businesses can adjust their pricing strategies to maximize profit, while policymakers can implement policies that promote economic stability and consumer welfare.

Types of Elasticity

Elasticity is a measure of the responsiveness of demand or supply to changes in price or income. There are several types of elasticity that economists use to analyze the behavior of consumers and producers in the market.

Price Elasticity of Demand

Price elasticity of demand measures the responsiveness of quantity demanded to a change in price. It is calculated as the percentage change in quantity demanded divided by the percentage change in price. If the price elasticity of demand is greater than 1, demand is considered elastic, meaning that a change in price will have a relatively large impact on quantity demanded. If the price elasticity of demand is less than 1, demand is considered inelastic, meaning that a change in price will have a relatively small impact on quantity demanded. If the price elasticity of demand is equal to 1, demand is unit elastic, meaning that a change in price will result in an equivalent percentage change in quantity demanded.

Income Elasticity of Demand

Income elasticity of demand measures the responsiveness of quantity demanded to a change in income. It is calculated as the percentage change in quantity demanded divided by the percentage change in income. If the income elasticity of demand is positive, a good is considered a normal good, meaning that as income increases, demand for the good also increases. If the income elasticity of demand is negative, a good is considered an inferior good, meaning that as income increases, demand for the good decreases. If the income elasticity of demand is zero, a good is considered income inelastic, meaning that a change in income will not have a significant impact on demand for the good.

Cross-Price Elasticity of Demand

Cross-price elasticity of demand measures the responsiveness of quantity demanded of one good to a change in the price of another good. It is calculated as the percentage change in quantity demanded of one good divided by the percentage change in the price of another good. If the cross-price elasticity of demand is positive, the goods are considered substitutes, meaning that as the price of one good increases, demand for the other good also increases. If the cross-price elasticity of demand is negative, the goods are considered complements, meaning that as the price of one good increases, demand for the other good decreases.

Price Elasticity of Supply

Price elasticity of supply measures the responsiveness of quantity supplied to a change in price. It is calculated as the percentage change in quantity supplied divided by the percentage change in price. If the price elasticity of supply is greater than 1, supply is considered elastic, meaning that a change in price will have a relatively large impact on quantity supplied. If the price elasticity of supply is less than 1, supply is considered inelastic, meaning that a change in price will have a relatively small impact on quantity supplied. If the price elasticity of supply is equal to 1, supply is unit elastic, meaning that a change in price will result in an equivalent percentage change in quantity supplied.