When it comes to making important economic decisions, having the right answers is crucial. Economic decision making involves assessing the costs and benefits of different options and choosing the one that will maximize value or minimize loss.

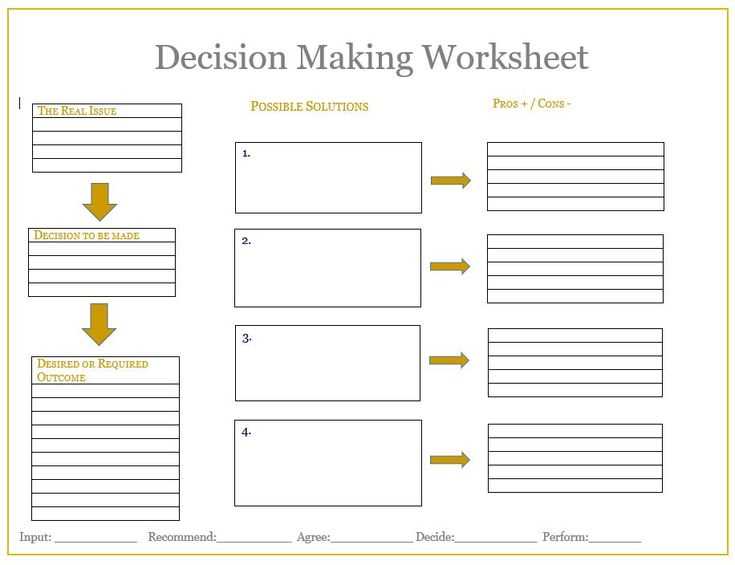

One tool that can help guide this decision making process is an economic decision making worksheet. This worksheet is a structured framework that prompts individuals or organizations to consider various factors related to a decision, such as available resources, potential risks, and expected outcomes.

By filling out this worksheet, decision makers can systematically analyze the pros and cons of each option, weighing the potential benefits against the associated costs. This process helps to minimize bias and subjectivity, providing a more objective assessment of the potential outcomes.

Ultimately, the purpose of an economic decision making worksheet is to support informed decision making by providing a clear and structured framework for analysis. By considering all relevant factors and using a systematic approach, decision makers can make more confident and successful economic decisions that align with their goals and objectives.

Economic Decision Making Worksheet Answers

Economic decision making is a complex process that involves weighing different options and considering various factors. A worksheet can be a helpful tool in organizing and analyzing information to make informed decisions. The economic decision making worksheet answers provide a framework for evaluating choices based on their costs and benefits.

One of the key questions in economic decision making is whether the benefits of a particular choice outweigh the costs. The worksheet helps individuals and businesses assess the potential gains and losses associated with different options. By considering factors such as financial costs, time commitment, and potential risks, decision makers can determine the most advantageous course of action.

The worksheet also encourages individuals and businesses to consider opportunity costs. This concept refers to the potential benefits that could have been gained by choosing an alternative option. By comparing the potential gains from different choices, decision makers can prioritize options and identify the most valuable opportunities.

Furthermore, the economic decision making worksheet answers help individuals and businesses assess the feasibility of different options. Considerations such as available resources, market conditions, and potential returns on investment play a crucial role in determining the viability of a particular choice. The worksheet prompts decision makers to think critically about these factors and make realistic evaluations.

In conclusion, economic decision making is a complex process that requires careful analysis and consideration. The use of a worksheet can facilitate this process by providing a structured framework for evaluating options. The economic decision making worksheet answers play a vital role in assessing costs, benefits, opportunity costs, and feasibility. By utilizing this tool, decision makers can make informed choices that align with their goals and optimize their resources.

What is Economic Decision Making?

Economic decision making is the process of making choices about how to allocate resources in order to meet economic goals and satisfy wants and needs. It involves evaluating various options and selecting the one that maximizes benefits or minimizes costs.

At the heart of economic decision making is the concept of scarcity. Resources such as land, labor, and capital are limited, while human wants and needs are unlimited. This creates a situation where individuals, businesses, and governments must make choices about how to use their scarce resources effectively and efficiently.

To make sound economic decisions, individuals and organizations rely on a variety of tools and principles. These may include analyzing costs and benefits, considering opportunity costs, using marginal analysis, and applying economic models and theories.

Cost-benefit analysis is a common tool used in economic decision making. It involves comparing the costs of a particular action or decision with the benefits that it will generate. By weighing the costs and benefits, individuals or organizations can determine whether the decision is worth pursuing.

Another important concept in economic decision making is opportunity cost. This refers to the value of the next-best alternative that is forgone when a choice is made. For example, if a person chooses to spend their money on a vacation, the opportunity cost may be the purchase of a new car. Understanding opportunity costs helps individuals and organizations make trade-offs and prioritize their choices.

Marginal analysis is also useful in economic decision making. It involves comparing the additional costs and benefits of a decision or action. By considering the marginal costs and benefits, individuals and organizations can evaluate whether the additional benefits outweigh the additional costs, and make an informed decision accordingly.

Overall, economic decision making plays a crucial role in our daily lives and in the functioning of the economy. It helps individuals, businesses, and governments make choices that can lead to efficient resource allocation, economic growth, and increased well-being.

Factors to Consider in Economic Decision Making

Economic decision making is a complex process that involves considering various factors before making a choice. These factors can have a significant impact on the outcome of an economic decision and can vary depending on the specific situation. Here are some key factors to consider:

1. Cost and Benefit Analysis: Before making any economic decision, it is important to analyze the costs and benefits associated with each option. This involves evaluating the potential costs involved in implementing a particular decision and comparing them to the expected benefits. By conducting a cost and benefit analysis, decision-makers can determine which option is the most financially viable and likely to result in the greatest overall benefit.

2. Opportunity Cost: Another important factor to consider is the opportunity cost of a decision. This refers to the value of the next best alternative that is forgone when a particular choice is made. By considering the opportunity cost, decision-makers can assess the potential benefits that could have been gained from choosing a different option.

3. Risk and Uncertainty: Decision-making in economics often involves a certain degree of risk and uncertainty. It is important to assess the potential risks associated with a decision and consider the likelihood of various outcomes. By considering the level of risk and uncertainty, decision-makers can make more informed choices and take appropriate measures to minimize potential losses.

4. Time Horizon: The time horizon of a decision is an important factor to consider, as it can impact the overall outcome. Some decisions may have short-term benefits but result in long-term drawbacks, while others may require an upfront investment but lead to long-term gains. By considering the time horizon, decision-makers can make choices that align with their long-term goals and objectives.

5. External Factors: Economic decisions are often influenced by external factors such as government regulations, market conditions, and social and environmental considerations. It is important to take these factors into account when making decisions, as they can have a significant impact on the outcome and sustainability of an economic choice.

In conclusion, economic decision making involves considering various factors such as cost and benefit analysis, opportunity cost, risk and uncertainty, time horizon, and external factors. By carefully evaluating these factors, decision-makers can make informed choices that align with their goals and objectives and result in the greatest overall benefit.

The Role of Opportunity Cost in Economic Decision Making

Economic decision making involves weighing the costs and benefits of different choices in order to make the best possible decision. One crucial concept in this process is opportunity cost. Opportunity cost refers to the value of the next best alternative that is forgone when making a decision. In other words, it is the cost of choosing one option over another.

Opportunity cost is an important consideration because resources such as time, money, and energy are limited. When making a decision, individuals and businesses must allocate these limited resources in the most efficient and effective way possible. By considering the opportunity cost, decision makers can assess the potential benefits and drawbacks of each option and make informed choices.

For example, imagine a business owner who is deciding whether to invest in expanding their production capacity or pursuing a new marketing campaign. The opportunity cost of investing in production capacity would be the potential benefits and profits that could have been generated from the marketing campaign. Similarly, the opportunity cost of the marketing campaign would be the potential increase in production capacity and efficiency that could have been achieved.

By considering the opportunity cost, the business owner can assess the potential gains and losses associated with each option. This analysis allows them to make a more informed decision based on their priorities and objectives. It also helps them to understand the trade-offs involved in their choices and to maximize the use of their available resources.

In conclusion, opportunity cost plays a crucial role in economic decision making. By considering the potential benefits and drawbacks of different choices, decision makers can evaluate the opportunity cost and make informed decisions that align with their goals and priorities. This analysis helps to maximize the efficient allocation of limited resources and ultimately leads to better economic outcomes.

Types of Economic Decisions

Economic decisions are choices made by individuals, businesses, or governments to allocate scarce resources in order to satisfy unlimited wants and needs. These decisions can be classified into different types based on their nature and purpose.

Individual Economic Decisions: Individuals make economic decisions every day, such as deciding how much to spend on groceries, whether to save or invest money, or whether to accept a job offer. These decisions are influenced by factors like personal preferences, income level, and current market conditions.

Business Economic Decisions: Businesses make economic decisions to maximize profits and ensure their long-term viability. These decisions may include choosing the optimal production levels, determining pricing strategies, deciding whether to expand into new markets, or evaluating investment opportunities. Businesses also make decisions regarding hiring and firing employees, as well as managing their supply chain and inventory.

Government Economic Decisions: Governments play a crucial role in the economy and make economic decisions to ensure stability and promote the overall welfare of society. These decisions may involve setting fiscal and monetary policies, regulating industries, providing public goods and services, imposing taxes, and redistributing income through welfare programs. The aim of government economic decisions is to achieve economic growth, reduce unemployment, and maintain price stability.

Investment and Financial Decisions: Investment and financial decisions involve the allocation of resources to different assets such as stocks, bonds, real estate, or retirement accounts. Individuals and businesses make these decisions based on factors like risk tolerance, return expectations, and future goals. These decisions can have significant impacts on personal wealth and business profitability.

International Economic Decisions: With the globalization of the economy, international economic decisions have become increasingly important. These decisions involve trade policies, foreign direct investment, exchange rate management, and international financial cooperation. Governments, businesses, and individuals make international economic decisions to maximize their benefits from global economic interactions and mitigate potential risks.

In conclusion, economic decisions are diverse and can vary depending on the context and the decision-maker involved. Whether it is an individual, a business, or a government, these decisions are essential for the allocation of scarce resources in a way that best satisfies the needs and wants of individuals and society as a whole.

Benefits and Risks of Economic Decision Making

When it comes to economic decision making, there are both benefits and risks involved. Making informed decisions can lead to positive outcomes, while uninformed decisions can have negative consequences.

Benefits:

- Profitability: Economic decision making allows individuals and businesses to assess the potential profitability of different options. By considering factors such as costs, revenues, and market trends, decision makers can identify opportunities for growth and success.

- Efficiency: Economic decision making helps optimize the allocation of resources. By evaluating costs and benefits, decision makers can allocate resources in a way that maximizes efficiency and minimizes waste.

- Rationality: Economic decision making encourages rational thinking and behavior. By analyzing information and weighing the pros and cons, decision makers can make logical choices that are based on evidence and reason.

Risks:

- Uncertainty: Economic decision making is often accompanied by uncertainty. Markets, consumer behavior, and external factors can change rapidly, making it challenging to predict outcomes accurately. This uncertainty increases the risk of making incorrect decisions.

- Opportunity cost: Economic decision making involves trade-offs and opportunity costs. Choosing one option often means forgoing another. Decision makers must carefully consider the potential benefits of each choice and the opportunity costs associated with the alternatives.

- External factors: Economic decision making is influenced by various external factors that are beyond the control of the decision makers. Factors such as government policies, economic conditions, and global events can impact the outcomes of economic decisions.

In conclusion, economic decision making has its benefits and risks. While it can lead to profitability, efficiency, and rationality, decision makers must also navigate uncertainty, opportunity costs, and external factors. By understanding these factors and making informed choices, individuals and businesses can increase their chances of making successful economic decisions.