In economics, one of the fundamental concepts is the production possibilities curve (PPC), which illustrates the different combinations of goods and services an economy can produce given its limited resources and technology. This curve showcases the trade-offs an economy must make in terms of allocating its resources between the production of different goods and services.

Chapter 1 section 3 of the economics textbook aims to provide a comprehensive understanding of production possibilities curves and how they can be used to analyze economic situations. As part of this section, students are typically given a worksheet with various questions related to the topic. These questions require them to apply the concepts learned and provide answers based on their understanding.

This article aims to provide answers to the worksheet questions that students may encounter in chapter 1 section 3 of their economics textbook. By providing detailed explanations and examples, this article can serve as a valuable resource for students seeking clarification and assistance in completing their worksheet tasks. Whether it’s calculating opportunity costs, understanding the concept of efficiency, or analyzing shifts in the production possibilities curve, this article will cover a range of essential topics.

Chapter 1 Section 3: Production Possibilities Curves Worksheet Answers

In Chapter 1 Section 3 of the economics textbook, students were introduced to the concept of production possibilities curves. These curves are graphical representations of the trade-offs an economy must make when allocating its limited resources between different goods and services. To assess students’ understanding of this topic, they were provided a worksheet with various scenarios and had to determine the different combinations of goods that can be produced using the given resources.

The answers to the production possibilities curves worksheet consist of a series of points along the curve that represent the maximum possible production of one good given the level of production of the other good. For example, if an economy can produce either 100 units of Good A or 200 units of Good B, the point (100, 200) would be part of the production possibilities curve.

Some of the answers to the worksheet may show a linear production possibilities curve, indicating a constant opportunity cost between the two goods. This means that the trade-off between producing more of one good and less of the other remains constant. Other answers may show a bowed-out production possibilities curve, indicating increasing opportunity costs. This suggests that the more of one good that is produced, the greater the amount of the other good that must be given up.

Overall, the production possibilities curves worksheet provides students with a hands-on opportunity to apply their knowledge of the concept and analyze different production possibilities. By understanding the limitations imposed by scarce resources, students can gain a better understanding of how societies must make choices when it comes to allocating resources and producing goods and services.

The Nature of Production Possibilities Curves

A production possibilities curve (PPC) is a graphical representation of the various combinations of two goods that an economy can produce given its available resources and technology. It shows the maximum amount of one good that can be produced for each possible level of production of the other good. The PPC is based on the concept of scarcity, which means that resources are limited and must be allocated efficiently.

The PPC is curved because of the concept of increasing opportunity cost. As an economy produces more of a particular good, the opportunity cost of producing an additional unit of that good increases. This is because resources are not equally suited to producing both goods, so as more resources are dedicated to one good, they become less available for producing the other good. This results in a trade-off between the production of the two goods, represented by the concave shape of the PPC.

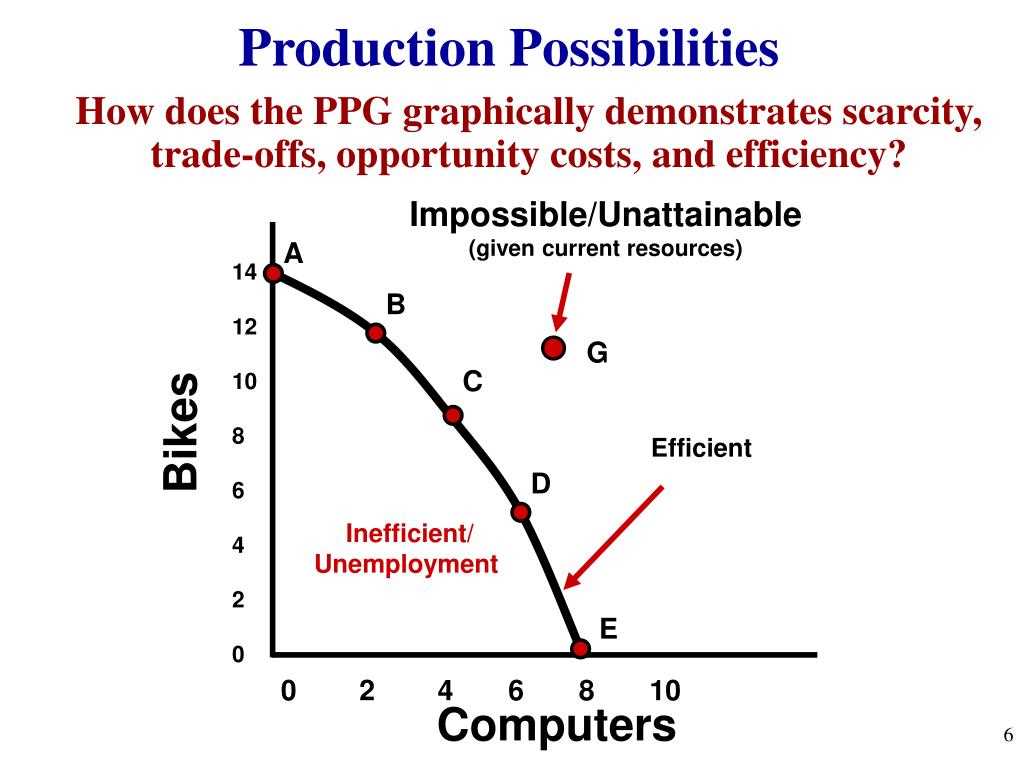

Points inside the PPC represent inefficient use of resources, as the economy is not fully utilizing its available resources. Points on the PPC represent efficient use of resources, as the economy is producing the maximum possible output given its available resources. Points outside the PPC are currently unattainable with the given level of resources and technology.

The PPC can shift outward or inward depending on changes in resources, technology, or the efficiency of resource allocation. An outward shift represents an increase in an economy’s productive capacity, while an inward shift represents a decrease. The PPC can also shift unevenly, indicating changes in the relative productivity of different goods.

In conclusion, the PPC is a visual representation of the trade-offs and opportunity costs faced by an economy in producing different goods. It illustrates the concept of scarcity and the need for efficient resource allocation. Understanding the nature of the PPC is essential for analyzing an economy’s production possibilities and making informed decisions regarding resource allocation.

Shifts in Production Possibilities Curves

Production possibilities curves (PPCs) are graphical representations of the different combinations of goods and services that an economy can produce given its limited resources. These curves illustrate the concept of trade-offs, as producing more of one good or service requires sacrificing the production of another. The PPC is typically drawn as concave to represent increasing opportunity costs.

Shifts in the PPC occur when there is a change in the economy’s available resources, technology, or efficiency. These shifts can be categorized as either inward or outward shifts. An outward shift of the PPC indicates an increase in an economy’s production capabilities, while an inward shift represents a decrease.

- Increase in available resources: If an economy discovers new natural resources or experiences a population growth, the PPC will shift outward. This means that the economy can produce more goods and services without sacrificing the production of other goods.

- Technological advancements: When there is an improvement in technology, the PPC will also shift outward. Technological advancements allow for greater efficiency in production, leading to an increase in the economy’s production possibilities.

- Inefficiency: Conversely, if there is a decrease in efficiency or if resources are being wasted, the PPC will shift inward. This indicates a decrease in the economy’s production capabilities.

It is important to note that shifts in the PPC do not happen instantaneously. They occur over time as an economy adjusts to changes in its resources, technology, and efficiency. Shifts in the PPC can have significant implications for an economy, influencing its output, employment levels, and overall economic growth.

Factors Affecting Production Possibilities

In order to understand the factors that affect production possibilities, it is important to first understand what a production possibilities curve (PPC) represents. A PPC shows the different combinations of goods that an economy can produce given its available resources and technology. It illustrates the trade-offs that occur when an economy chooses to allocate its resources to the production of one good over another. However, the position and shape of the PPC can be influenced by a variety of factors.

1. Resources: One of the most significant factors influencing production possibilities is the availability and quality of resources. The types and quantities of resources, such as land, labor, capital, and entrepreneurship, determine the range of goods that can be produced. For example, an economy with abundant natural resources may have a larger production capacity for goods related to mining or agriculture.

2. Technology: Technological advancements have a direct impact on production possibilities. Improved technology can increase an economy’s efficiency and productivity, allowing it to produce more goods with the same amount of resources. For instance, the invention of new machinery or production techniques can lead to an outward shift of the PPC, indicating an expansion of production possibilities.

3. Trade: International trade can also affect production possibilities. By engaging in trade, an economy can access goods and resources that it is unable to produce domestically. This can lead to an increase in production possibilities as the economy can specialize in producing the goods in which it has a comparative advantage.

4. Economic System: The type of economic system in place can influence production possibilities. In a centrally planned economy, where the government controls resource allocation, production possibilities may be limited due to inefficiencies or lack of incentives. In contrast, a market economy, where resources are allocated based on supply and demand, may allow for greater flexibility and potential growth in production possibilities.

Overall, a variety of factors can shape and influence a nation’s production possibilities. Understanding these factors is crucial in analyzing an economy’s potential for growth and development.

Opportunity Cost in Production Possibilities Curves

In the study of production possibilities curves, one important concept that is often discussed is the concept of opportunity cost. Opportunity cost refers to the cost of forgoing the next best alternative when making a decision. In the context of production possibilities curves, opportunity cost can be seen as the trade-off between producing one good over another.

When we examine a production possibilities curve, we can see that it represents the different combinations of two goods that an economy can produce using its available resources and technology. Every point on the curve represents a specific allocation of resources to produce a certain quantity of each good. However, producing more of one good means producing less of the other good, and this is where opportunity cost comes into play.

As an economy moves along the production possibilities curve, it must make choices about how to allocate its limited resources. For example, let’s say an economy can produce either 10 units of Good A or 20 units of Good B. If it decides to produce 10 units of Good A, the opportunity cost is the 20 units of Good B that could have been produced instead. Similarly, if it decides to produce 20 units of Good B, the opportunity cost is the 10 units of Good A that could have been produced.

Opportunity cost is important because it helps us understand the trade-offs that societies face when allocating their resources. By analyzing the production possibilities curve and considering the opportunity costs involved, we can make more informed decisions about resource allocation and understand the limits of what can be produced given a set of resources.

Efficiency and Inefficiency in Production Possibilities Curves

Production Possibilities Curves (PPCs) are graphical representations that illustrate the different combinations of goods or services an economy can produce when it efficiently utilizes its resources. These curves show the trade-offs an economy faces when allocating its resources between different goods or services.

An economy is considered efficient if it is producing at a point on the PPC curve, where it is maximizing its output given the available resources. Any point along the PPC curve represents efficient production levels because resources are fully utilized and allocated in the best possible way.

- Efficient points: Points on the PPC curve indicate that an economy is producing its maximum potential output given its resources.

- Inefficient points: Points inside the PPC curve indicate that an economy is not fully utilizing its resources. It is producing below its potential output.

- Unattainable points: Points outside the PPC curve indicate that an economy does not have enough resources to produce at those levels of output. These points are currently unattainable given the available resources.

When an economy is operating at an inefficient point, it implies that resources are being wasted or underutilized. This could be due to factors such as unemployment, inefficient allocation of resources, or inadequate technology. In such cases, the economy has room for improvement by reallocating resources or improving productivity to reach a more efficient point along the PPC curve.

Understanding efficiency and inefficiency in production possibilities curves helps economists and policymakers analyze an economy’s potential and make informed decisions to enhance production levels. By identifying inefficiencies, policymakers can implement strategies to improve resource allocation, technological advancements, and overall economic performance.

Interpreting Production Possibilities Curves

A production possibilities curve (PPC) is a graphical representation of the trade-offs a society faces when allocating its scarce resources between different goods and services. The curve shows the maximum combinations of goods that can be produced given the available resources and technology.

When analyzing a PPC, there are several key points to consider:

- Efficiency: Points that lie on the PPC represent efficient combinations of goods, where resources are fully utilized. Points inside the PPC indicate inefficient use of resources, while points outside the PPC are currently unattainable with the given resources and technology.

- Trade-offs: The PPC illustrates the concept of trade-offs between different goods. As more resources are allocated to the production of one good, the production of the other good decreases. This reflects the opportunity cost of producing one good over another.

- Opportunity Cost: The opportunity cost of producing one unit of a good is the amount of the other good that must be given up. The slope of the PPC represents the opportunity cost, as it shows the rate at which one good can be substituted for another.

By analyzing a PPC, economists and policymakers can gain insights into the efficiency of an economy and the trade-offs that arise from resource allocation decisions. This understanding can help inform economic policy and guide decision-making to maximize societal welfare.